The General Department of Taxation (GDT) issued the Instructions on the Procedures for Implementing Tax Incentives under the Special Program to Promote Investment in Sihanouk Province.

In accordance with the Instruction No. 29722 dated on 12 Sept

ember 2025, which follows Decision No. 07 dated on 10 January 2024, the Royal Government of Cambodia launched the Special Program to Promote Investment in Preah Sihanouk Province, effective until the end of 2025.

ember 2025, which follows Decision No. 07 dated on 10 January 2024, the Royal Government of Cambodia launched the Special Program to Promote Investment in Preah Sihanouk Province, effective until the end of 2025.

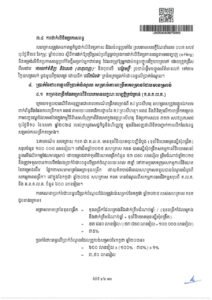

Under the program, investors seeking to benefit from tax incentives must submit applications to the Sihanoukville Investment Promotion Team via Secretariat in either Sihanoukville or Phnom Penh. Upon receiving approval in principle from the relevant ministry, investors are required to complete tax registration though they are exempted from patent tax and registration fees. Unregistered enterprises must register through the Secretariat using prescribed forms (Forms 101-P2 to 101-P5), while registered enterprises can use their existing Tax Identification Numbers (TINs). Enterprises with multiple projects must obtain separate TINs for each approved project. Essential registration documents include the Tax Registration Certificates (VAT and Patent), Tax Identification Card, Patent, Notification of Fiscal Obligations, and the official letter confirming receipt of tax benefits under the Special Program.

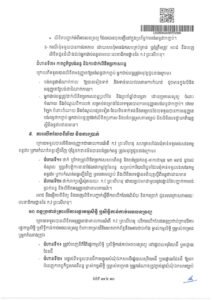

Once registration is complete, the Tax Office issues a tax exemption letter allowing investors to proceed under specific tax categories. These cover exemptions and incentives related to withholding tax on real estate rentals, zero percent VAT for local suppliers and inputs, income tax exemptions for new and expanding projects, minimum tax, billboard tax, packaged tax payments, stamp duty, and property tax. Notably, property tax exemptions are granted automatically and remain valid until the expiration of the incentive period, eliminating the need for annual declarations. Investors must also comply with monthly or annual filing obligations via the GDT’s online system or mobile application. Monthly declarations require entering business data and payments or requesting state-burden receipts if exempt, while annual declarations through the “ToI e-Filing” system accordingly.